P U B L I C I D A D E

Surpassing the more optimistic expectations

Real estate financing with resources coming from savings accounts reached in 2013 a new historical record of expenditures: R$ 109.2 billion

The year of 2013 had excellent results in the areas of savings, credit and real estate market. These results only now start to be disclosed.

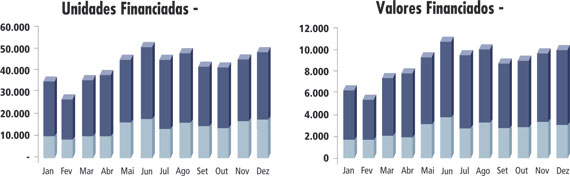

According to the Brazilian Association of Institutions of Real Estate Credit and Savings (Abecip), property financing with resources coming from savings accounts reached a new historical record in expenditures, with a total of R$ 109.2 billion. These figures represented an increase of about 32 percent if compared to 2012, when the disbursements totalized R$ 82.8 billion. Abecip data do not include loans with resources coming from the Mandatory Fund for Unemployment Benefit (FGTS) such as the loans for the program My House, My Life. Only in December, 2013, R$ 10.4 billion were paid, corresponding to an increase of 17 percent in relation to the same month of 2012.

The volume of loans for buying and constructing properties only in December, 2013 was of R$ 10.4 billion. This represents an increase of 2.3 percent on the results of November and, if compared with the same month of the former year, an increase of 17 percent.

These figures were a surprise even for Abecip, that was expecting for 2013 an increase of 15 percent in disbursements. For Octavio de Lazari Junior, president of Abecip, 40 percent of this result was due to the increase in real estate prices. The remaining 60 percent represent the real increase of financing disbursements.

Along 2013, 529,800 properties were financed with resources from savings accounts, showing an increase of 17 percent over the former year. In 2012 the number of financed unities was of 492,900. And once more considering only December as a reference, we have 50,900 properties bought and built—an increase of 7 percent on November values and of 19 percent if referred to the same month of 2012.

According to the president of Abecip, several factors related to the macroeconomic scenario contributed for this unique performance, such as low level of unemployment, increase in people income and—most of all—a huge increase in the offer of the resources available in savings accounts.

From January to December, 2013, the total of savings accounts deposits in the Brazilian System of Savings and Loans reached R$ 466 billion, 20 percent above the total accumulated from January to December, 2012. The liquid capitation of savings accounts was above R$ 54 billion, corresponding to an increase of 46 percent if compared to the accumulated value of 2012.

Only in December, 2013, the deposits in savings accounts were R$ 8.3 billion above the withdrawals. This was the best result in a single month since July, 1994. In December, 2012, the net capitation of savings was of R$ 6.9 billion.

Another factor that influenced the results was the low level of default, about 1.8 percent in 2013 “We have the lowest default rate of the whole Brazilian bank system. Default is under complete control and in a descending path,” said Lazari Junior.

Sales increasing

A research carried out by Abecip showed that the increase of credit in 2013 was driven by financing operations to buy real estate. In other words, Brazilian people caused an increase of 41 percent in the quantity of property financing, totalizing R$ 76.9 billion of the total disbursement of R$ 109.2 billion.

A research carried out by Abecip showed that the increase of credit in 2013 was driven by financing operations to buy real estate. In other words, Brazilian people caused an increase of 41 percent in the quantity of property financing, totalizing R$ 76.9 billion of the total disbursement of R$ 109.2 billion.

Disbursements for construction were of R$ 32.3 billion, corresponding to an increase of 15 percent on the values of 2012.

Abecip expects a new increase of credit during this year. According to its president, the expectance is an increase of approximately 15 percent, corresponding to a total of R$ 126 billion, what will be a new historic record.

No fear of the bubble

Lazari Junior discarded the possibility of a bubble in the market, as occurred in the United States and Europe, shaking their economy. “The bubble is formed in the moment that the agents buy properties expecting increase in their value instead of work based on the real market prices”, says him.

Besides the low rates of default in the sector, he points out that Brazilian borrower enters usually with 30 to 35 percent of the property value in owner resources when contracting the financing. This fact would help by itself to compose funding for real estate credit. According to him, this funding is composed by resources from savings accounts (60 percent) and from Mandatory Fund for Unemployment Benefit – FGTS (40 percent).

Another factor to be considered--according to the president of Abecip—is that 95 percent of the properties in Brazil are bought for living and not for investment. “The typology of the Brazilian consumer is quite different,” says him.

At the end he points out that there are rigid criteria for property financing in Brazil, such as a maximum limit of 80 percent of its total value, instead of more than 100 percent, as occurred in European countries, where financing for furniture and home appliances were also given.

About property prices, Lazari Junior stated that—after the strong rising of last years—they will remain stable from now on. “Prices will remain stable, except in one or other area of instability,” said him. “What we feel is that the financed value is being coherent with the increase in value that occurs in the neighborhood."

The possibility of creation of a property bubble in Brazil was also discarded by Bain & Company, global business consultant that published the study Risk of bubble or growing impeller? which compares Brazil with seven countries selected in accordance with the high resilience or high impact that they showed in the recent economic crisis. These countries (Germany, Canada, Spain, United States, Ireland, Portugal and United Kingdom) were also compared among them.

In its study, Bain believes that besides the perception of price rising, several other indicators have to be followed to better define if a property bubble exists or does not exist, as well as the potential dimensions of its development and of what would trigger its explosion. Besides analyzing this process, the consultant verified also the behavior of a borrower of property financing in moments of crisis.

Considering all countries studied, a situation that is common among those which more suffered with the property crisis was remarkable: the unreal expectation of continuous rising of property values. This belief leaded people to invest blindly in the real estate market, forcing a more speculative increase in the prices and the creation of a dangerous property bubble because it separates prices from the basis of supply and demand.

Considering all countries studied, a situation that is common among those which more suffered with the property crisis was remarkable: the unreal expectation of continuous rising of property values. This belief leaded people to invest blindly in the real estate market, forcing a more speculative increase in the prices and the creation of a dangerous property bubble because it separates prices from the basis of supply and demand.

For Brazil, the main conclusion is that we are not in a property bubble. On the other hand, there are some critical indicators that have to be evaluated and followed to identify prematurely the creation of a bubble. When default rises, the bubble would be blown up and then will be too late.

According with the supplied material, there are five relevant factors to better understand the principles of generation of a property bubble:

1.Conditions offered for property credit, measured by the percent value of the property to be financed (known as Loan-to-value ratio or LTV);

2.Periods of financing payment and approval processes of property financing;

3.Affordability to the acquisition of a property (affordability ratio);

4.Penetration of property credit as percent of the GDP;

5.Commitment level of family income.

“Our conclusion is that Brazilian numbers are much near of those of the countries that better resisted to the crisis—such as Germany—than of the numbers of the countries that had strong impacts with the crisis, such as Spain, Ireland and United States. Nevertheless, the high level of income commitment in Brazil and the accelerated increase of property values if compared to family income suggest attention to the evolution of these indicators,” states Rodolfo Spielmann, partner of Bain & Company and author of the study.

Av. Francisco Matarazzo, 404 Cj. 701/703 Água Branca - CEP 05001-000 São Paulo/SP

Telefone (11) 3662-4159

© Sobratema. A reprodução do conteúdo total ou parcial é autorizada, desde que citada a fonte. Política de privacidade